If you’re installing a heat pump in Australia, you’re already making one of the smartest moves for long-term energy bills. Heat pumps are ridiculously efficient, but they do shift more of your home or business running costs onto electricity. That’s where solar and batteries start to look seriously attractive, especially when you want to run heating, cooling, or hot water into the evening and early morning.

The tricky part is how you pay for the battery.

Most people end up choosing between two “money savers” that sound similar but work very differently: a solar battery rebate that reduces the upfront price, or an interest-free loan that spreads repayments out over time.

In Australia right now, the biggest battery support is the Australian Government’s Cheaper Home Batteries Program, which provides around a 30% discount on eligible small-scale battery systems connected to new or existing rooftop solar. That discount is delivered through the Small-scale Renewable Energy Scheme, often applied by your installer or retailer as part of your quote.

In Victoria, there’s another twist: Solar Victoria’s interest-free battery loan is no longer taking new applications, so for many locals the real comparison becomes rebate versus other finance options rather than rebate versus the old state loan.

What’s the actual difference between a solar battery rebate and an interest-free loan?

A rebate reduces the cost of the battery system you’re buying. In plain terms, it’s a discount that shows up on the invoice or quote, so you’re paying less from day one.

An interest-free loan doesn’t reduce the sticker price. It makes the purchase easier to afford by spreading the cost into monthly repayments, ideally without interest. That can be brilliant for cashflow, but it’s only “better” if the loan really is fee-light and suits your budget.

The big mindset shift is this: rebate is about paying less overall, while interest-free finance is about paying more slowly. They can sometimes be used together, but it depends on the program rules and the finance provider.

What battery rebate is available in Australia now, and how does it work?

The main national support is the Cheaper Home Batteries Program, which provides around a 30% discount on eligible batteries from 1 July 2025.

It’s delivered through the Small-scale Renewable Energy Scheme using Small-scale Technology Certificates, often shortened to STCs. The usual customer experience is simple: your installer or retailer handles the certificate side and you see the value as a discount in your quote, rather than having to lodge forms yourself.

One important detail for anyone trying to time their project is how the program defines “installed”. Under the program guidance, a battery is considered installed when the electrical compliance certificate is issued, or the state equivalent. That date matters for eligibility.

Also worth knowing: the discount level can change over time because the STC settings can be adjusted. The Clean Energy Regulator has flagged changes to keep the discount roughly around 30% while costs shift, with more frequent adjustments.

Is there a solar battery rebate in Ballarat, or is it different because I’m regional?

For most households and small businesses, the solar battery rebate in Ballarat works the same way as it does across Australia, because it’s a federal program delivered nationally through the same scheme.

What does change in Ballarat is not the rebate rules, but the value you get from a battery once it’s installed. Ballarat’s cooler winters often mean higher heating demand, which is exactly why heat pump owners love batteries: you can store daytime solar and use it later when heating is doing the heavy lifting. The better your battery matches your evening and morning load, the more you can reduce grid imports at peak times.

So when locals ask, “Is the Ballarat rebate different?”, the better question is usually, “How do I size the system so the rebate turns into real savings?”

What does “battery rebate in Victoria eligibility” mean?

When people search for battery rebate eligibility in Victoria, they’re usually trying to confirm whether they qualify for the federal battery discount, and whether their battery and installer qualify too.

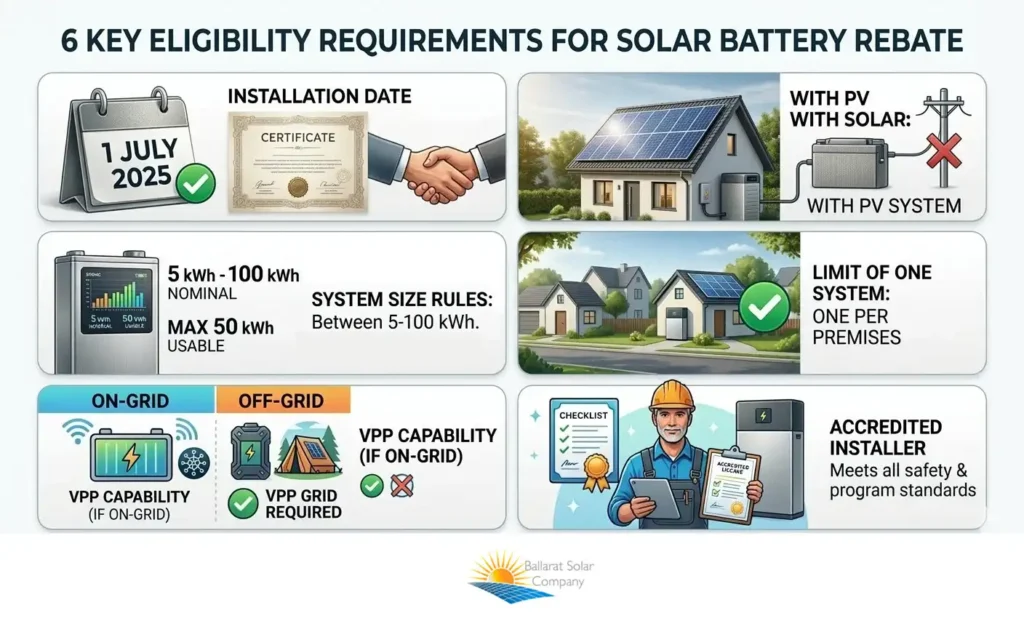

Here are the key requirements that matter most:

- The battery must be installed on or after 1 July 2025, based on the electrical compliance certificate date.

- The battery must be installed with a new or existing solar PV system. Batteries installed without solar, storing only grid electricity, are not eligible.

- The battery must fit the size rules. The Clean Energy Regulator explains that eligible batteries must be between 5 kWh and 100 kWh nominal capacity, and STCs can only be claimed for up to 50 kWh of usable capacity.

- Only one battery system per premises is eligible for STCs.

- On-grid batteries generally need to be VPP capable, meaning able to communicate and respond to signals, although they do not have to actually join a VPP. Off-grid systems don’t need to be VPP capable.

- Installation needs to meet safety and accreditation requirements, and the program guidance points to accredited battery installation pathways.

It sounds like a lot, but it usually boils down to three practical checks: your battery is the right kind, it’s installed the right way, and the paperwork is done properly.

Are interest-free loans for batteries still available in Victoria?

As of the latest Solar Victoria guidance, Solar Victoria is no longer taking applications for interest-free loans for the installation of a battery system.

That’s important because many Victorians still talk about “the battery loan” as if it’s an ongoing option. If you already applied earlier, Solar Victoria’s page outlines the process for final approval and repayment details. But for new battery buyers in 2026, the practical comparison is usually:

- Federal discount through the Cheaper Home Batteries Program, and

- Whatever finance options you can access privately, such as green loans, bundled retailer finance, or business lending.

The good news is you can still plan a battery project around the federal discount. The “loan versus rebate” decision simply becomes “do I pay the reduced price upfront, or do I finance the reduced price over time?”

Can I stack a rebate and a loan, or do I have to pick one?

In many real-world installs, people end up using both types of support, just not always through the same program.

With the federal battery discount, you typically don’t apply to the department yourself. The discount is commonly delivered through the installer or retailer using STCs, and you see it in the quote.

Because it’s applied at the point of sale, you can often still choose to finance what’s left, depending on the finance provider’s rules. The main thing is to confirm the finance terms are based on the post-discount price, and that there aren’t hidden fees that quietly eat into the benefit.

For heat pump buyers, stacking can be especially appealing because you might be upgrading more than one thing at once: hot water, space conditioning, induction cooking, maybe an EV charger later. Getting the battery discount first, then financing the remainder, can keep the whole electrification plan manageable.

Which one is better financially, the rebate or the interest-free loan?

If we’re talking pure dollars, a rebate usually wins because it reduces the purchase price immediately. Paying less up front means you’re not “carrying” the full cost, and the savings start on day one.

But money is not just about totals. It’s also about timing.

An interest-free loan can be better if paying upfront would force you into a smaller battery than you actually need, or if you’d otherwise delay the project for years. A battery that is working for you now, helping run your heat pump through winter peaks, can be more valuable than the perfect battery you never get around to installing.

The smartest way to compare is to line up two scenarios and keep them brutally simple:

First scenario: you pay the discounted price upfront and start saving straight away.

Second scenario: you finance the discounted price and measure whether the monthly repayments feel comfortable compared to your expected bill reductions.

If you’re a business, add one extra layer: batteries can also help with peak usage management, which can matter depending on your tariff and demand structure. Even then, the decision still comes back to the same thing: total cost versus cashflow comfort.

Does choosing a rebate versus a loan change what battery I should install?

It can, and this is where people accidentally make expensive mistakes.

When someone is focused on getting the rebate, they sometimes aim for the cheapest eligible battery rather than the right-sized battery. That can lead to a system that fills up too early or doesn’t cover the evening usage they expected, which reduces the real-world payoff.

When someone is focused on repayments, they sometimes stretch to a bigger battery because the weekly or monthly number feels acceptable. Later, they realise the battery is underused, or the repayments feel annoying during months when bills are already higher.

The smarter approach is to size the battery based on your usage pattern first, then choose the funding method that makes that sensible system achievable. In other words, don’t let the finance option dictate the design. Let the design dictate the finance option.

For businesses, it can also be worth thinking about how a battery supports operational hours, peak usage, and consistency. A battery that is matched to how your site uses power will deliver better value than one chosen mainly because it fits a loan limit or looks good with a discount headline.

What should I check before I commit, so I don’t lose the rebate or get stuck with a bad loan?

Whether you’re leaning rebate or a loan, the biggest win is avoiding surprises. Most regrets come from unclear eligibility, unclear pricing, or unclear finance terms.

Start with clarity on the rebate side. Make sure the battery and installation meet the program rules, and ask your installer to explain how the discount is applied in the quote. You’re not trying to do their job for them, you’re just making sure the discount you’re expecting is actually built into the numbers you’re comparing.

Then look at the loan side, if you’re considering finance. Confirm the total amount repayable, any fees, what happens if you want to pay it out early, and whether the finance is tied to any specific product or contract conditions. Interest-free can be great, but the fine print is what decides whether it stays great.

Finally, compare apples with apples. Put the rebate-discounted upfront price next to the rebate-discounted financed price, and ask one simple question: Does the convenience of repayments outweigh any extra cost or restrictions? If yes, finance may be the right move. If not, paying upfront after the rebate will usually feel cleaner.

Solar Battery Rebate vs Interest-Free Loan - what’s better?

For many homeowners and small businesses, a rebate-style discount is often the better option in pure dollars because it reduces what you pay straight away. If you can afford the upfront cost after the discount, it’s usually the simplest path with fewer ongoing commitments.

An interest-free loan can be the better option when cashflow matters more than paying the lowest total price, or when you want to install a properly sized system now instead of postponing the project. It becomes a good choice only when the repayments are genuinely comfortable and the terms are transparent.

In Victoria, it’s also important to know that Solar Victoria’s interest-free battery loan is no longer taking new applications, so many people now compare the federal discount against other finance options available to them.

If you want help working out what option suits your property, talk to a local Ballarat Solar Company. A good local team can explain the solar battery rebate in Ballarat, check battery rebate in Victoria eligibility where relevant, and design a system that makes financial sense, whether you pay upfront or choose finance.

Ready to move forward? Get in touch with Ballarat Solar Company for solar battery installation in Ballarat for a clear quote that makes the rebate and finance options easy to compare.